Diabetes, a special program

How many times do we encounter clients with small health issues, who want some form of life insurance coverage? It happens all the time. Diabetes, as an example, is one health issue that arises more often than not, and can sometimes rear its ugly head when clients get older. Fortunately, Diabetes is not an automatic decline, and many times we can get clients coverage at a reasonable offer/premium. However, for those older clients (60 and above), paying an increased premium on a term policy might not be all that attractive. The thought of paying a higher premium and not having any payoff on the backend can be troubling to some clients. Here is a possible alternative:

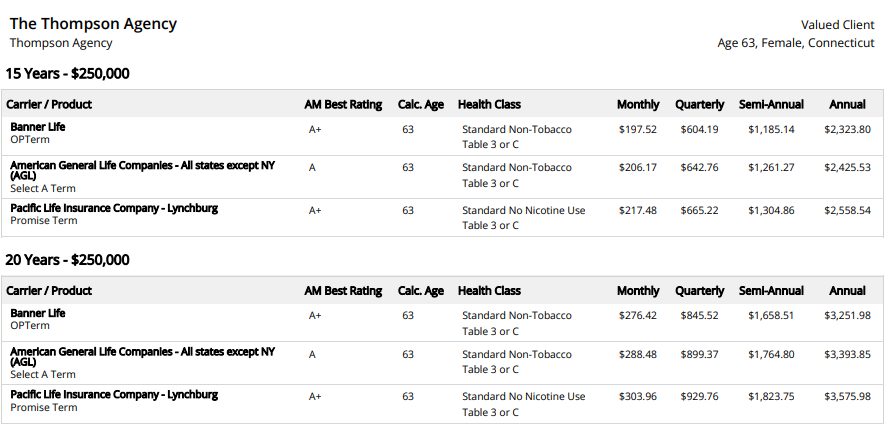

Case Study

Here is a case study where we can utilize a special program, called table reduction, using a Lincoln permanent policy as an alternative to paying a rated premium on term. Let’s assume this 63-year-old female is looking for $250,000 in coverage. She has diabetes type II and has kept it under decent control. However, it has ultimately been concluded that she will receive a table C. A 20-year level term with Banner at table C will require her to pay a premium of $3,251 over the next 20 years (most competitive carrier at table C). The client could certainly choose this option as it does represent the lowest of pocket cost for the coverage. However, Lincoln has a table reduction program, where any client who receives up to a table C rating will automatically be upgraded to standard non-tobacco on any of their permanent products. Click HERE for pricing below

This same client could pay $5,061 per year and have that same $250,000 guaranteed till age 90, with the potential to have the policy carry for lifetime @ 5.7%. In addition, in 20 years, there would be $110,872 of cash surrender value. This is versus total premiums paid of $101,220. The client could choose to surrender the policy and receive this 110% ROP. She could choose to keep the coverage going. It leaves the client with many options that she wouldn’t have had with a term policy. And lastly, the client is locking in a standard non-tobacco rating where this will hopefully be the last life insurance policy she ever has to purchase. Click the illustration below for details.