LifeLinc – Leveraging qualified plan for Wealth Transfer

Do you have any clients with the bulk of their wealth in qualified plans such as 401(k), 403(b), or 457? Do these same clients have children? And is leaving money to them a priority?

With the SecureAct eliminating stretch IRA’s, leaving money to the next generation through a qualified plan or IRA is less efficient than ever before.

Plan Goal

Here is a great presentation that any of our agents/advisors can put together fairly easy for any client who owns a qualified plan. The goal of this presentation is not to steer the client towards buying life insurance, but it is rather an analysis to determine what strategy best fits their needs & wishes. The idea is to show the client a side-by-side comparison of them keeping the status quo, continuing to grow their qualified plan, and then eventually take required minimum distributions. The presentation even offers the options of showing the client reinvesting RMD’s and assuming a specific growth rate (would be same growth rate assumed on the qualified plan itself) or spending down RMD’s.

Full Presentation

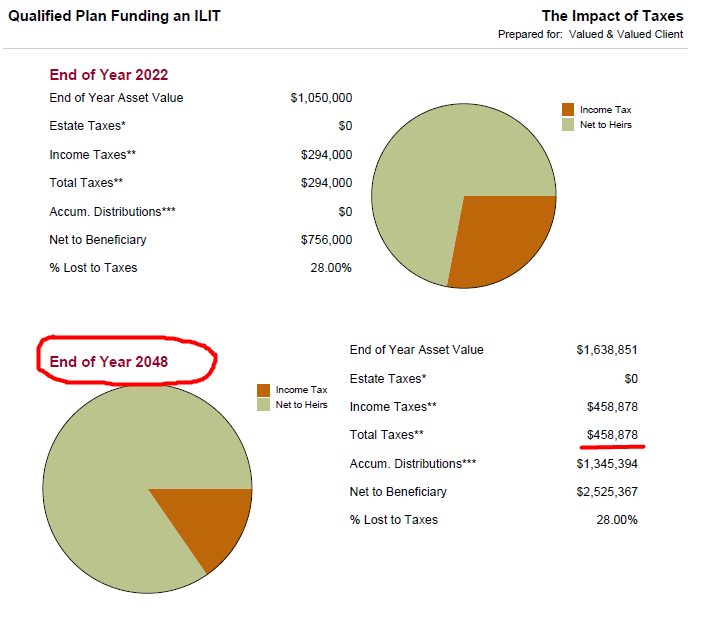

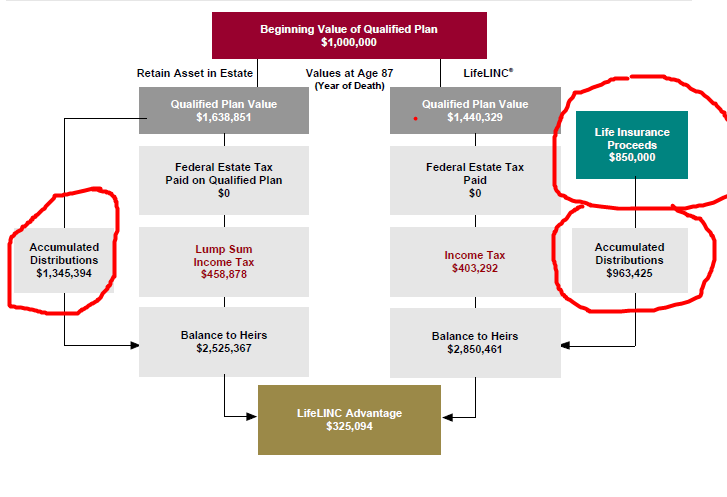

The full presentation (see attached), is fairly lengthy but it really has something for every type of client/agent. There are reports (ledgers) that show how these values are determined, while the snapshots below are not as detailed but still do a great job of showing how life insurance can be way to transfer assets more tax efficiently. The first snapshot shows what would happen to his/her qualified plan if it was to grow at a 5% growth rate, with RMDs happening at age 72. Most tax conscious clients should be shocked at the amount of tax that would be owed on their qualified plan, especially since almost every other asset left to heirs receives a step up in cost basis at death. That is not the case with qualified plans, and hence it decreases the value of what is left to loved ones.

On this example, it shows the following

- The owner of $1M qualified plan can take a $13,888 distribution each year, and use the net proceeds of $10,000 to pay premium on 2nd to Die Lincoln IUL (assuming 28% tax bracket)

- Assuming a standard non-tobacco rating on the 61-year old male and a preferred rating on the 61-year old female, that $10,000 will purchase $850,000 of tax free 2nd to Die death benefit.

- $850,000 guaranteed till age 95, with coverage for lifetime at 5.74%

- Clients are able to almost replace the current value qualified plan and assure that a level tax free benefit is left to their children, without taking away from their own retirement.